Cancellation vs Nonrenewal in Car Insurance: What’s the Difference?

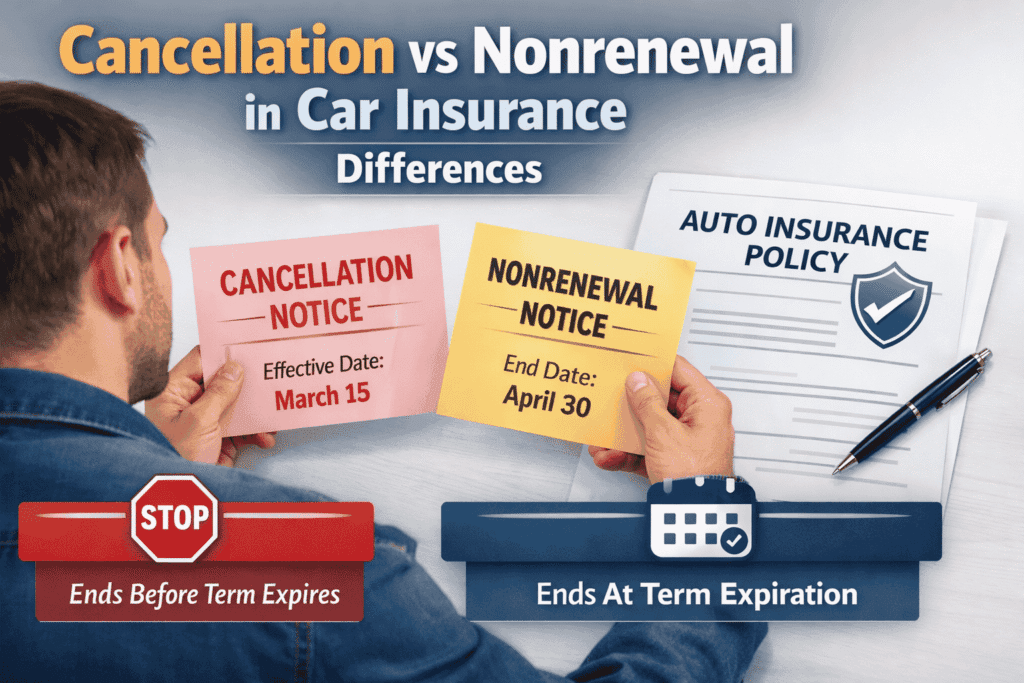

Cancellation vs nonrenewal in car insurance confuses many drivers because both can end a policy, but they do not usually mean the same thing. In simple terms, cancellation usually means the policy ends before the current term is over, while nonrenewal usually means the insurer decides not to continue the policy when the current term expires.

That difference matters more than it sounds. A mid-term cancellation can leave a driver scrambling to avoid a coverage gap, while a nonrenewal often gives more time to shop for another policy before the expiration date arrives. If you want the broader foundation first, it helps to review cancel car insurance, because ending a policy voluntarily is different from an insurer ending or not renewing it.

This guide explains what cancellation and nonrenewal usually mean, how they work in real life, why the difference affects your next steps, and what to check in your policy and notices before coverage ends.

Quick summary

- Cancellation usually means a policy ends before the current term expires.

- Nonrenewal usually means the insurer will not continue the policy after the current term ends.

- The timing, notice, and next steps can be different for each one.

- Either situation can create a coverage gap if you do not act in time.

- The most important things to check are the effective date, the stated reason, and what you need to do next.

What cancellation vs nonrenewal means

A simple way to separate the two is to ask one question: is the policy ending before the term ends, or at the end of the term?

Cancellation usually means the policy is being ended before the expiration date shown on the declarations page. That can happen for different reasons depending on the stage of the policy, the state, and the policy terms.

Nonrenewal usually means the policy stays active through the end of the current term, but the insurer chooses not to offer another term after that point.

Many drivers treat both words like they simply mean “my insurance is ending,” but the timeline matters. A cancellation often requires a faster response. A nonrenewal usually gives more runway, even though it can still create problems if you wait too long to replace the policy.

How each one can happen in real life

In practice, the difference becomes clearer through everyday situations.

Imagine a driver misses premium payments and does not fix the problem by the date shown in the notice. In that kind of situation, the insurer may cancel the policy before the term ends. Now imagine a different driver reaches the end of a six-month or twelve-month term and receives notice that the insurer will not continue the policy for the next term. That is usually a nonrenewal instead.

Drivers are often surprised because the notice can look like just another insurance document. That is why it helps to know how to read a car insurance policy and related notices, especially the effective date, the reason given, and whether the document says cancellation, expiration, or nonrenewal.

Another real-life difference is urgency. With cancellation, the question is often, “How many days do I have before the policy stops?” With nonrenewal, the question is usually, “How long do I have to line up the next policy before this one expires?”

Why the difference matters

The main reason it matters is simple: a coverage gap can create bigger problems than many drivers expect. Even a short gap can affect registration, lender requirements, future shopping, and what you may pay next time.

Cancellation can feel more disruptive because it may happen during an active policy term. Nonrenewal can still be stressful, but it often gives you more time to prepare. That timing difference changes what your next step should be and how quickly you need to act.

This can also turn into a cost issue. A driver who waits too long after a cancellation or nonrenewal may end up with fewer options or a harder time finding similar coverage again. That is one reason it helps to understand what affects car insurance cost before replacing a policy in a hurry.

Common reasons for cancellation or nonrenewal

Not every notice happens for the same reason. In many cases, the reason depends on timing, policy terms, underwriting rules, and state requirements.

- Cancellation may happen after missed payments, missing documents, or other issues that affect the current policy term.

- Nonrenewal may happen because of underwriting changes, claim history, risk changes, or the insurer’s decision not to continue that type of policy.

- The exact reason and notice rules can vary by state and by policy language.

That is why the notice itself matters more than assumptions. The most useful first step is to read the stated reason carefully and confirm the exact end date of the current coverage.

What to check before your policy ends

If you receive a notice, slow down and review the details carefully. A short checklist helps:

- Check the effective date. Find out exactly when the current coverage ends.

- Read the stated reason. Do not assume it is obvious from the envelope or email subject line.

- Confirm whether the notice says cancellation or nonrenewal. That changes your timeline.

- See whether any action can still change the outcome. In some situations, a payment issue or missing information may still be fixable before the deadline.

- Make sure there is no coverage gap. If you need a replacement policy, line it up before the end date.

- Keep the document. Save the notice with your policy records in case you need the dates later.

The most useful mindset is practical, not emotional. Whether the policy is being cancelled mid-term or not renewed at expiration, the real priority is understanding the timing and protecting continuity of coverage.

Conclusion

Cancellation and nonrenewal both lead to the end of an auto policy, but they usually do it at different points in the policy timeline. Cancellation usually means the policy ends before the current term is over. Nonrenewal usually means it ends when the term expires and will not continue into the next one.

The difference matters because it affects how much time you have, what documents to review, and how urgently you need to arrange the next step. Once you know which one you are dealing with, the path forward becomes much easier to understand.

Related articles

- Cancel Car Insurance: Can You Do It Anytime?

- How to Read a Car Insurance Policy: Sections Made Simple

- What Affects Car Insurance Cost? 11 Key Factors

FAQ

Is cancellation worse than nonrenewal?

Not always, but cancellation is often more urgent because it usually ends the policy before the current term is over.

Does nonrenewal mean my policy was cancelled?

Usually no. Nonrenewal generally means the policy stays active until the end of the current term but will not continue into the next one.

Can I still drive after a cancellation notice arrives?

What matters is the effective date in the notice. Coverage usually continues until that date, not forever after the notice arrives.

What is the most important thing to check first?

Start with the effective end date, then confirm whether the notice is for cancellation or nonrenewal and what reason is listed.