Higher deductible lower premium is a common idea in car insurance, and it often comes up when your bill increases or you are trying to adjust your coverage. The logic sounds simple: if you agree to pay more out of pocket after a claim, the insurer may charge less for the policy. If you’re here because your price jumped, it can help to read Why Is My Car Insurance So Expensive? first.

But it does not work the same way for every driver or every type of coverage. A higher deductible can reduce the cost in some situations, yet it can also increase your financial risk when something goes wrong. If your question is more “are insurers allowed to raise prices like this?”, see Insurance Rate Increase Legal? What the Rules Allow.

In this guide, you will learn what a deductible really is, when changing it can affect your premium, and how to think through the tradeoffs in a practical, everyday way.

Definition / Core concept

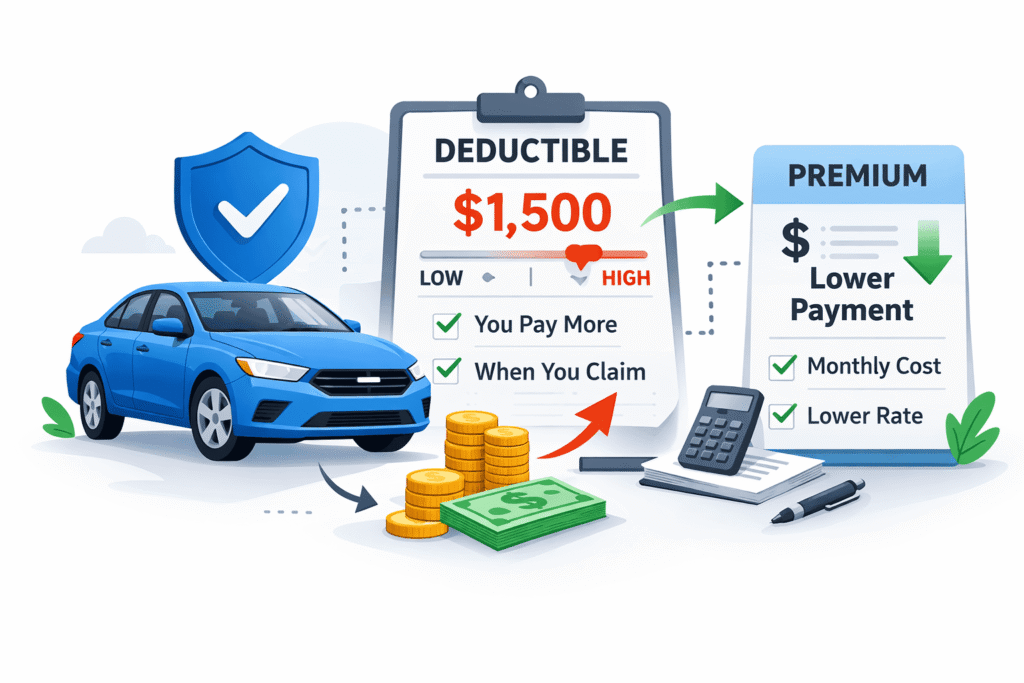

A deductible is the amount you pay out of pocket on a covered claim before your insurance coverage pays the remaining approved costs. Deductibles usually apply to certain coverages, not all of them. For a full beginner-friendly overview, see What Is a Deductible in Car Insurance?.

Simple example: if your collision deductible is $1,000 and you have a covered accident with $4,000 in repair costs, you generally pay the first $1,000 and the insurer pays the remaining $3,000 (after claim approval and any limits).

So why do people say a higher deductible can lower your premium? Because the deductible is one way you share risk with the insurer. When you take on more of the first part of a loss, the insurer may take on less overall risk, which can lower the premium in many cases. To understand what your policy is actually responsible for (and what it is not), see What Does Car Insurance Cover?.

How it works in practice

Changing a deductible is usually a policy-level adjustment you can request at renewal, and sometimes mid-term (rules depend on the insurer and state). Here is how it typically works:

- You choose a coverage to adjust. Most often, this is collision and comprehensive.

- You select a deductible option. Common options include several set amounts (not a custom number).

- The insurer recalculates risk. Higher deductible means you pay more in a claim, which can reduce expected payouts.

- Your premium may change. Many policies show a lower premium with a higher deductible, but the size of the change can vary a lot.

- Your out-of-pocket risk changes immediately. If you have a claim tomorrow, the new deductible is what you may owe.

It is important to separate two things: the premium (what you pay to keep the policy active) and the deductible (what you may pay if you file a covered claim). A lower premium can feel helpful month to month, but a higher deductible can be a bigger financial hit when repairs are needed. If you’re filing a claim (or thinking about it), this overview helps: Car Insurance Claims Process.

Main types, coverage, or variations

Deductibles are most common on physical damage coverages. The effect of changing them depends on which part of the policy you are talking about.

Collision coverage

Collision helps pay to repair or replace your car after a crash with another vehicle or object (like a pole), regardless of fault in many cases. Collision usually has a deductible. Raising the collision deductible is one of the most direct ways people try to lower premium on a policy. If you’re comparing collision to other “damage to your car” coverage, see Collision vs. Comprehensive Insurance.

Comprehensive coverage

Comprehensive (sometimes called “other than collision”) usually covers damage from events like theft, vandalism, fire, falling objects, or weather-related damage. Comprehensive also usually has a deductible. In many policies, you can choose a different deductible for comprehensive than for collision.

Liability coverage

Liability generally pays for injuries or property damage you cause to others. Most auto liability coverage does not use a deductible the way collision and comprehensive do. So, changing deductibles typically does not apply to liability in the same direct way. If you want a simple comparison, see Liability vs. Full Coverage.

Uninsured/underinsured motorist and PIP/MedPay

These coverages vary by state. Some may have deductibles, some may have different cost-sharing rules, and some may not use deductibles at all. The key point: the “raising your deductible can lower your premium” relationship is strongest and most predictable with collision and comprehensive.

Costs or influencing factors (if applicable)

Even if the general idea is true, several factors affect how much a higher deductible changes a premium (and whether it changes it much at all):

- Your driving and claims history: Prior claims, tickets, or accidents can weigh more than deductible choices.

- Vehicle value and repair costs: More expensive repairs can change how the insurer prices collision and comprehensive risk.

- Where you live and park: Local crash rates, theft risk, and weather patterns can affect comprehensive and collision pricing.

- Coverage limits and add-ons: Other policy choices can move the premium up or down more than the deductible does. (Related: Car Insurance Policy Limits.)

- Financing or leasing rules: A lender or lease agreement may require collision and comprehensive and may limit how high the deductible can be.

- Your ability to pay the deductible: This is not a pricing factor, but it is a real-world factor that should guide your decision.

Deductibles are only one pricing lever—this guide explains the bigger picture: What Affects Car Insurance Cost?.

Also, keep in mind that lowering your premium is only one part of the picture. A higher deductible can reduce the number of claims that make sense to file. For smaller losses near the deductible amount, you might choose to pay out of pocket instead of filing.

That can be good or bad depending on your situation. It can reduce paperwork and avoid small claims, but it can also leave you paying more when you need repairs quickly.

Common questions or misunderstandings

Does a higher deductible always mean a lower premium?

Often, but not always. Many policies do price higher deductibles with lower premiums for collision and comprehensive, but the change may be small. Other rating factors can outweigh it.

If I choose a very high deductible, is my coverage worse?

The coverage type is usually the same, but your out-of-pocket cost is higher when you file a claim. That can make the coverage feel less helpful for moderate losses.

Will a higher deductible lower premium for liability coverage too?

Usually no, because liability coverage typically does not work with a deductible in the same way. Deductible changes are most relevant for collision and comprehensive.

Can I have different deductibles for collision and comprehensive?

Many policies allow it. For example, a driver might choose a higher collision deductible and a lower comprehensive deductible, depending on risk and budget.

Do I pay the deductible even if the accident is not my fault?

For your own collision claim, you may still pay your deductible first, depending on how the claim is handled. In some situations, your insurer may later recover money from the at-fault party (a process called subrogation), and deductible reimbursement rules vary.

Is it smart to raise my deductible to avoid filing claims?

It can reduce the number of smaller claims that might not be worth filing. But it only makes sense if you can comfortably pay the higher deductible when you truly need to use the coverage.

Important to Know

Car Policy Answers is an independent educational website. We do not sell insurance, provide quotes, or recommend insurance companies.

The information in this article is intended for general educational purposes only and is based on publicly available insurance guidelines and common industry practices.