Liability vs full coverage is a common question because these terms are used in very different ways. One driver may say they “only have liability,” while another says they have “full coverage,” but the real difference usually becomes clear only after an accident or a claim. To understand the basics first, see What Is Car Insurance and How Does It Work?.

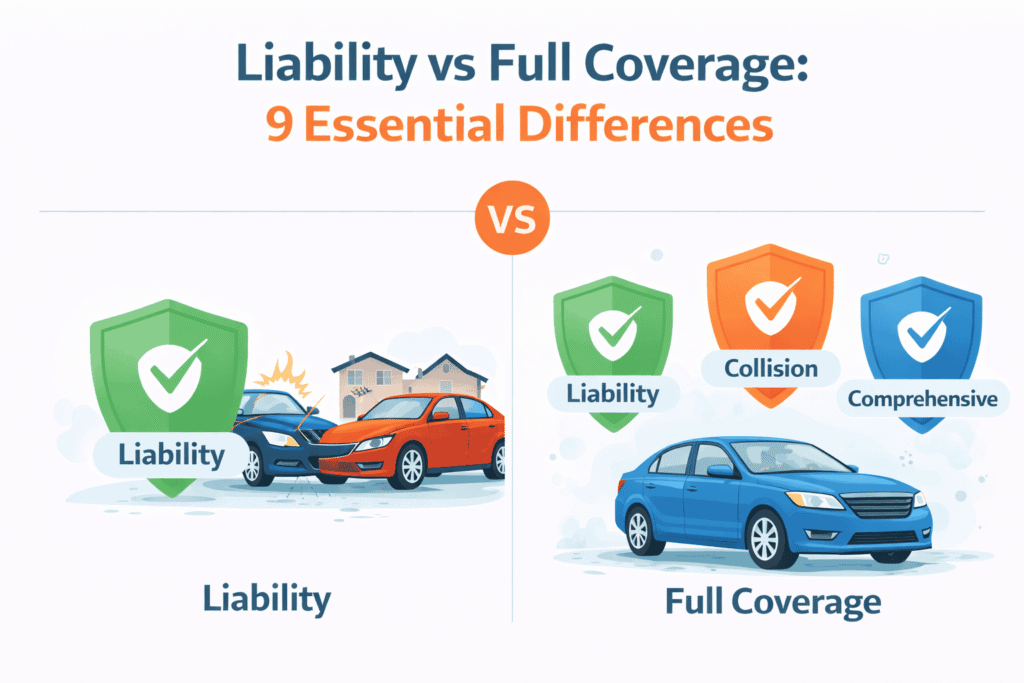

In simple terms, liability coverage is mainly about paying for damage or injuries you cause to other people. Full coverage is a common phrase (not an official policy type) that usually means you also have coverage for your own car, such as collision and comprehensive.

This article explains liability vs full coverage in plain language, with examples and the key details to check on your declarations page so you know what protection you actually have.

Liability vs full coverage: the simple definition

Liability insurance generally helps pay for injuries and property damage you cause to others in an accident. It usually does not pay to repair your own vehicle.

Full coverage is a common phrase people use to describe a policy that includes liability plus coverage that can help pay for damage to your own car, most often:

- Collision coverage (crash damage to your car)

- Comprehensive coverage (non-crash damage like theft, hail, vandalism, fire, or hitting an animal)

Simple example: If you rear-end another car, liability coverage may help pay for the other driver’s repairs. If your own front bumper is damaged, liability typically won’t pay to fix your car. Collision coverage is the part that usually helps with your vehicle repair in that situation.

How it works in practice (what gets paid)

When a loss happens, the claim is handled under the coverage that matches the type of damage. Here’s the typical flow:

- Identify what was damaged

Was it someone else’s car/property, your car, injuries, or all of the above? - Match the damage to the right coverage

- Liability usually applies to other people’s damage and injuries (if you caused the accident).

- Collision usually applies to crash damage to your own car (if you carry it).

- Comprehensive usually applies to non-collision damage to your own car (if you carry it).

- Apply policy rules

Limits, deductibles, exclusions, and claim facts determine what is covered.

The biggest difference is this: liability protects other people, while “full coverage” usually means you also have protection for your own vehicle in more situations.

Liability vs full coverage: 9 key differences

Use these differences to understand what you have and what your policy may actually pay for.

1) Who is protected

Liability coverage is mainly for damage or injuries to other people. Full coverage usually means you also have coverage that may protect your own car.

2) Damage to your own car

With liability-only, damage to your own car is often not covered by your policy. With “full coverage,” collision and comprehensive may help pay for repairs or a total loss (depending on policy terms).

3) Crash vs non-crash losses

Collision is generally for crash damage (hitting a car or object). Comprehensive is generally for non-crash losses (theft, hail, vandalism, fire, falling objects, animal impacts).

4) Deductibles

Deductibles usually don’t apply to liability claims. Collision and comprehensive usually have deductibles, meaning you pay part of the covered loss out of pocket before insurance pays.

5) Policy limits (and what they cap)

Liability limits cap what the insurer can pay for other people’s injuries and property damage. Collision and comprehensive have their own limits and are also affected by the vehicle’s value and policy rules.

6) What the law usually requires

Most states require at least liability coverage to legally drive. Collision and comprehensive are usually optional under state law.

7) Lenders and leases

If you finance or lease your car, your lender commonly requires collision and comprehensive. That’s one reason many drivers end up with what people call “full coverage.”

8) Common exclusions

Liability, collision, and comprehensive all have exclusions and conditions. For example, policies often do not cover routine maintenance, mechanical breakdown, normal wear and tear, or intentional damage.

9) What “full coverage” really means

“Full coverage” is not a standardized legal term. Two drivers can both say they have full coverage and still have different limits, deductibles, and optional coverages. The declarations page is the best place to confirm what you actually have.

What to check on your declarations page

If you want to quickly confirm liability vs full coverage on your own policy, look for these items on your declarations page (dec page):

- Liability limits (bodily injury and property damage)

- Collision (listed as included or not) and the collision deductible

- Comprehensive (listed as included or not) and the comprehensive deductible

- Any optional coverages (uninsured motorist, MedPay/PIP, rental reimbursement)

If collision and comprehensive are missing, you likely have liability-only (or something close to it). If they are included, you likely have what many people call full coverage.

Common questions and misunderstandings

Is full coverage required by law?

Usually no. Most states require liability coverage (and some require additional protections). Collision and comprehensive are often optional unless a lender requires them.

Does liability insurance fix my car?

Typically no. Liability usually pays for damage you cause to others. Damage to your car is usually handled under collision or comprehensive if you carry them.

Does full coverage mean everything is covered?

No. Policies still have limits, deductibles, exclusions, and conditions. “Full coverage” usually means more types of coverage are included, not that coverage is unlimited.

Important to Know

Car Policy Answers is an independent educational website. We do not sell insurance, provide quotes, or recommend insurance companies.

The information in this article is intended for general educational purposes only. Coverage rules vary by state and policy, and claim outcomes depend on the facts of the loss.