Knowing how to compare two car insurance policies line by line can help you avoid a very common mistake: choosing the cheaper option without noticing that the protection is not really the same. Two policies can look similar at first glance and still work very differently after an accident, theft, hail claim, or lawsuit.

In practice, the premium is only one part of the decision. What usually matters more is how the policies compare in liability limits, deductibles, physical damage coverage, endorsements, exclusions, and extras like rental reimbursement or roadside assistance.

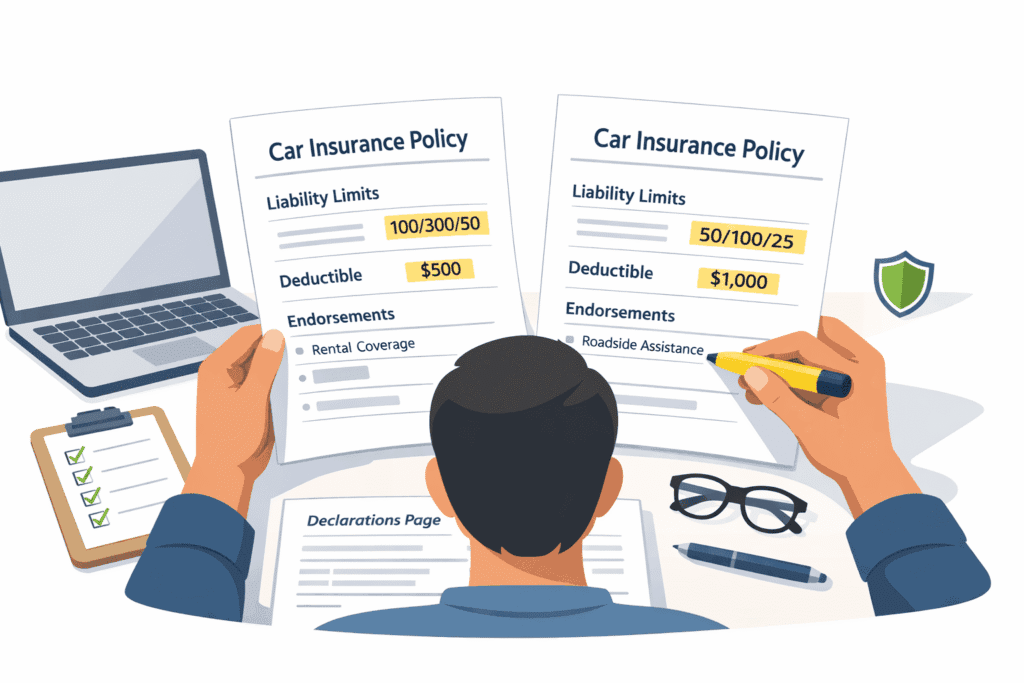

This guide breaks the process into simple steps so you can compare both policies side by side without getting lost in insurance language. If you need a broader overview first, it helps to start with how to read a car insurance policy before judging which version is stronger.

- Compare the same vehicle, drivers, and address before reviewing price.

- Check liability limits first, because that is where protection differences can be large.

- Look at deductibles and covered perils, not just whether collision or comprehensive appears.

- Review endorsements, exclusions, and optional coverages line by line.

- Use the declarations page as your starting point, then confirm details in the full policy.

- A lower premium is not always the better value if the policy shifts more risk back to you.

Start by making the comparison fair

Before you compare anything, make sure both quotes or policies are built on the same facts. A side-by-side review only works when the policies are based on the same car, the same drivers, the same garaging address, and similar usage. If one version assumes lower annual mileage, excludes a driver, or removes rental coverage, the price difference may not reflect better efficiency. It may simply reflect less protection.

A good first step is to place both declarations pages next to each other. This page usually summarizes the core details: named insured, covered vehicles, key coverages, deductibles, limits, and endorsements. It is the fastest way to see whether you are truly comparing the same thing.

When the basics match, move through the policy in this order:

- Liability coverage limits

- Collision and comprehensive coverage

- Deductibles

- Uninsured or underinsured motorist coverage

- Medical payments or personal injury protection, where applicable

- Optional coverages and endorsements

- Exclusions and claim-related conditions

Compare the parts that change your financial risk

Many drivers go straight to the premium. A better approach is to begin with the sections that determine how much risk stays with you after a loss.

Liability limits: These limits affect how much the policy may pay if you cause injury or property damage to others. One policy may look cheaper because it carries meaningfully lower limits. That difference may not matter during a minor scrape in a parking lot, but it can matter a lot in a serious accident. If you want a deeper breakdown, this guide on car insurance policy limits helps clarify what those numbers mean in real life.

Collision and comprehensive: Do not stop at whether these coverages exist. Check whether both policies include them, whether deductibles match, and whether one version has narrower terms. A policy with a much higher deductible can reduce the premium while increasing your out-of-pocket cost later.

Uninsured or underinsured motorist coverage: This can matter when the other driver has little or no insurance. If one policy includes stronger protection here, that may be more valuable than a small premium difference.

Optional add-ons: Rental reimbursement, roadside assistance, glass coverage, accident forgiveness, custom equipment, and similar options are easy to overlook. This is also where car insurance endorsements can change what the policy actually does. One version may include helpful extras automatically, while another may leave them out entirely.

Look for what is missing, limited, or excluded

Good comparison is not only about what appears on the page. It is also about what has been removed, narrowed, capped, or conditioned.

For example, two policies may both say they include rental reimbursement. But one may only pay a lower daily amount or stop sooner. Two policies may both include roadside assistance, but one may limit the number of uses. The same thing can happen with towing, windshield claims, transportation expenses, or aftermarket parts language.

You should also read the exclusions and conditions. In practice, this is where surprises often hide. A policy may exclude certain drivers, business use, rideshare use, custom parts beyond a set amount, or losses tied to specific situations. Some differences are not deal-breakers, but they should be visible before you choose.

How this works in real life

Imagine two policies for the same car. Policy A costs less each month. Policy B costs more. At first, Policy A seems like the better deal. But then you compare them line by line.

- Policy A has lower liability limits.

- Policy A uses a higher collision deductible.

- Policy A does not include rental reimbursement.

- Policy A has fewer endorsements and narrower optional benefits.

Now imagine your car is damaged and needs repairs for two weeks. With Policy B, the claim may leave you with less out-of-pocket cost and fewer transportation problems. That does not automatically make Policy B the right choice for everyone, but it shows why a lower premium does not always mean better value.

Another common example is comparing one policy renewal with a new quote. If the new version looks cheaper, check whether it lowered limits, raised deductibles, changed covered drivers, or removed endorsements. What seems like savings can sometimes be a different product altogether.

What to check before you choose one policy

- Are the drivers, vehicle, address, and usage details identical on both versions?

- Do the liability limits match closely enough for a fair comparison?

- Are collision and comprehensive deductibles the same?

- Does one policy include stronger uninsured motorist protection?

- Are rental, towing, glass, or roadside benefits included or removed?

- Are there endorsements or exclusions that change how the policy works?

- Does the cheaper option leave you carrying more financial risk after a claim?

If the answer to any of those questions is unclear, keep reading before making a decision. Insurance comparisons are most useful when you can explain not just which policy is cheaper, but why it is cheaper.

Conclusion

The best way to compare two car insurance policies line by line is to go beyond premium and review the parts that shape real protection: limits, deductibles, physical damage coverage, uninsured motorist protection, endorsements, exclusions, and practical extras. That is what shows whether the lower price reflects efficiency or reduced coverage.

A calm, side-by-side review usually makes the differences easier to see. When you compare the same facts, read the declarations page first, and check the policy details that affect your out-of-pocket risk, the decision becomes much clearer.

Related articles

- How to Read a Car Insurance Policy: Sections Made Simple

- What Is a Declarations Page (Dec Page) in Car Insurance?

- Car Insurance Policy Limits: What They Mean and How They Work

FAQ

Is the cheaper car insurance policy usually worse?

Not necessarily. But it may include lower limits, higher deductibles, fewer extras, or more restrictive terms. That is why the line-by-line review matters.

What is the most important line to compare first?

Liability limits are a strong place to start because they can change your financial exposure in a major accident. After that, review deductibles and optional coverages.

Can two policies have the same coverages but still work differently?

Yes. They may differ in deductibles, endorsements, exclusions, payment limits, or claim conditions. The names can look similar even when the details are not.

Should I compare the declarations page or the full policy?

Start with the declarations page because it gives you a quick summary. Then confirm the details in the full policy, especially for exclusions, endorsements, and optional coverages.