Driving without insurance can create much bigger problems than many drivers expect. Some people realize their policy lapsed after a missed payment. Others are between cars, switching insurers, or assume they do not need coverage for a short time. But once a vehicle is on the road, the consequences of being uninsured can become expensive very quickly. If you want the basic foundation first, start with What Is Car Insurance?.

In many states, the issue is not just financial. It can also affect registration, license status, and what happens after a crash. The exact rules vary, which is why there is no single national penalty chart that fits every driver. Still, some consequences show up again and again when people are caught driving without insurance.

This guide explains 10 things that can happen, why the risk is bigger than just a ticket, and what to do if you realize you are currently uninsured.

Quick summary

- Driving without insurance can lead to fines, registration problems, and major out-of-pocket costs after a crash.

- The exact penalties vary by state, but many drivers also face administrative headaches beyond the initial ticket.

- If you cause damage or injuries without insurance, you may have to pay personally.

- A lapse can also affect future underwriting and make it harder or more expensive to get insured again.

- If you realize you are uninsured now, the safest move is usually to stop driving until coverage is active again.

Can you get in trouble for driving without insurance?

In many places, yes. The exact outcome depends on state rules, whether the vehicle is registered, and what happened while the vehicle was uninsured. If you are unsure about the legal baseline, this guide on whether car insurance is required in the U.S. helps explain the bigger picture.

The important thing to understand is that uninsured driving risk is not limited to one bad day. What begins as a lapse or missing proof of coverage can turn into fines, suspended registration, personal liability after a crash, and future insurance complications.

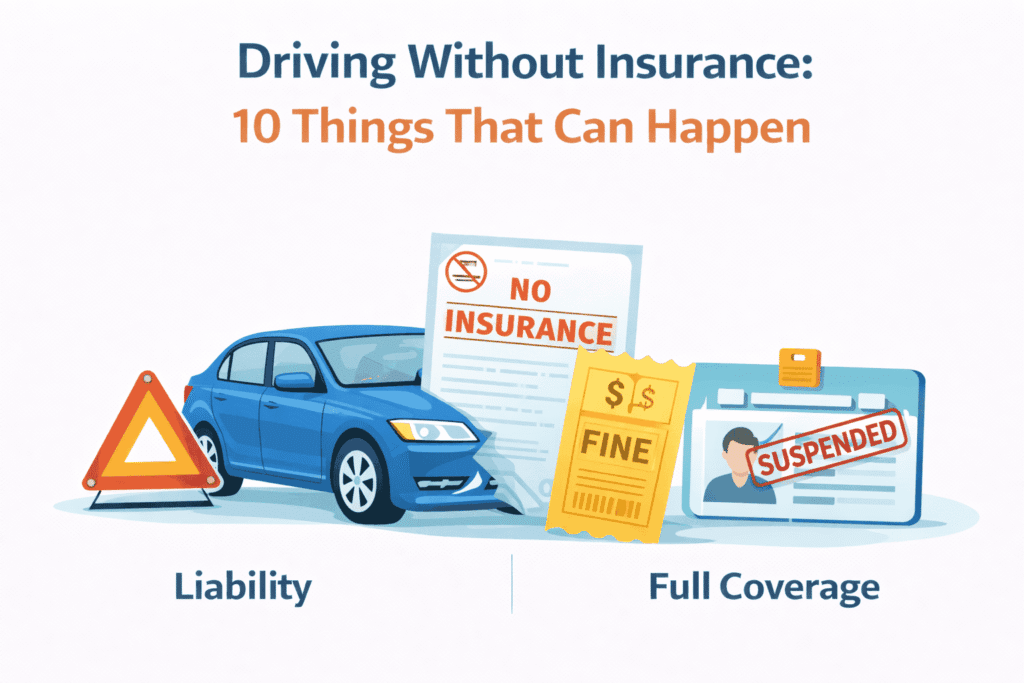

10 things that can happen if you drive without insurance

- You may get a ticket or fine.

One of the most common outcomes is a citation for failing to carry required coverage or proof of financial responsibility. In some states, the fine may rise for repeat issues. - Your registration may be suspended.

Some states connect insurance status directly to vehicle registration. If coverage lapses or proof is missing, the state may flag the registration. - Your driver’s license may be affected.

Depending on the situation and state rules, uninsured driving can lead to license suspension or reinstatement requirements. - Your car may be towed or impounded.

In some cases, especially after a stop or traffic incident, the vehicle itself may be taken off the road. - You may have to pay out of pocket after a crash.

If you cause damage to another car, building, or person, there may be no insurer paying on your behalf. That can turn a routine accident into a major personal financial problem. - You may be personally responsible for injuries.

Medical expenses can be one of the most expensive parts of an accident. Without liability coverage, those costs may fall directly on you if you are legally responsible. - You may face court or collection problems.

If the other party seeks payment and there is no insurance handling the claim, the dispute can move into collections, lawsuits, or judgments depending on the facts. - You may need extra filings to get back on the road.

Some drivers may later need proof-of-insurance filings or other state-required steps before driving legally again. - Future insurance may become harder or more expensive.

A lapse can affect future underwriting. Even when a driver gets coverage again, the new policy may not look the same as before. - A simple mistake can turn into a long administrative mess.

Missed notices, canceled registration, billing confusion, reinstatement fees, and timing mistakes can all make the problem last longer than expected.

Why a crash without insurance can get expensive fast

Many drivers think the biggest risk is the ticket. In practice, the larger danger often appears after an accident. When a covered driver causes a crash, the policy may help handle liability within its limits. When an uninsured driver causes the same crash, there may be no policy stepping in on that person’s behalf.

That can mean paying for vehicle damage, injuries, towing, storage, or other losses directly. And if you are wondering how the process normally works when coverage is active, this guide to the car insurance claims process helps show what is missing when no policy is there to respond.

Even a relatively minor accident can feel much more serious when there is no insurance layer between the driver and the financial consequences.

What to do if you realize you are uninsured right now

If you just discovered that your policy lapsed or was canceled, the safest response is usually simple and immediate.

- Stop driving the vehicle until coverage is active again.

- Check whether the policy truly lapsed or whether it is a billing or document issue.

- Review the cancellation date and any notices carefully.

- Make sure registration status and lender requirements are still being handled properly.

- When coverage resumes, confirm the effective date in writing.

Some drivers assume they can solve the problem tomorrow and still use the car today. That is where the biggest avoidable risk usually begins.

Common misunderstandings about driving without insurance

“If I only drive a short distance, it does not matter.”

No. A short trip can still lead to a stop, a crash, or another event that exposes the problem.

“I have no loan, so insurance no longer matters.”

Not necessarily. State law, registration rules, and liability risk can still matter even without a lender.

“If I never have an accident, being uninsured saves money.”

That ignores ticket risk, lapse consequences, and the possibility of one loss causing much larger costs than the premium ever would have.

“A one-day lapse is too small to matter.”

Sometimes even a short lapse can still create underwriting, administrative, or legal issues depending on the situation.

The bottom line

Driving without insurance can lead to much more than a simple fine. Depending on the state and the situation, it may affect your registration, license, future insurance options, and your personal finances after a crash. The biggest risk is often not the stop itself, but what happens if something goes wrong while no active coverage is in place.

If you think your policy may have lapsed, do not assume it can wait. Check the status, confirm the dates, and avoid using the vehicle until you know coverage is active again. If the lapse happened because the old policy ended unexpectedly, this guide on canceling car insurance can help you understand timing, gaps, and what to check next. That one step can prevent a small policy problem from turning into a much bigger one.

Related topics

- What Is Car Insurance?

- Is Car Insurance Required by Law in the U.S.?

- Car Insurance Claims Process: 9 Steps That Really Happen

FAQ

Can you go to court for driving without insurance?

It can happen, especially if an uninsured crash leads to a dispute over damages or if state enforcement rules escalate the issue beyond a simple citation.

Can your registration be suspended for no insurance?

In many states, yes. Some systems connect active insurance status to vehicle registration, so a lapse may create registration problems.

Will a lapse make future insurance more difficult?

It may. A lapse can affect future underwriting and may change how a new insurer views the risk.

What should I do if I find out my insurance already lapsed?

The safest step is usually to stop driving the vehicle, verify the policy status, and confirm new or restored coverage before using the car again.