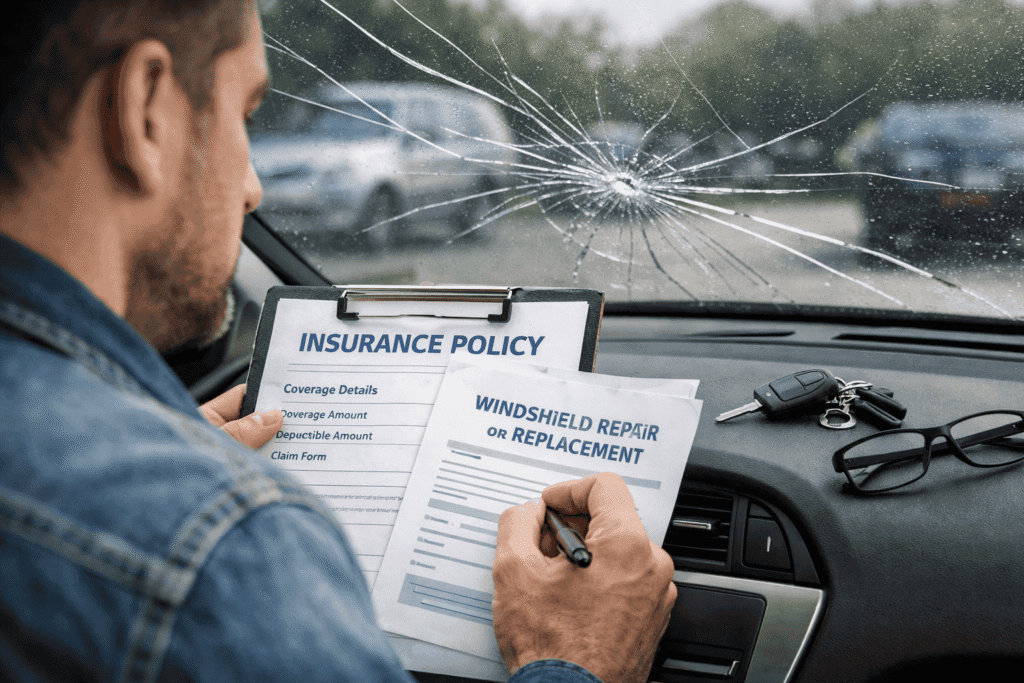

A cracked windshield can happen fast. A small rock hits the glass on the highway, a long crack appears, and suddenly you are wondering whether your insurance helps with the repair bill. The short answer is: sometimes. Whether car insurance covers windshield replacement usually depends on what caused the damage and which coverage you carry.

In many cases, windshield replacement is handled under comprehensive coverage, but not every policy works the same way. Some policies may cover full replacement, some may only help after a deductible, and some may not help at all. It also matters whether the glass can be repaired instead of replaced.

This guide explains when windshield replacement is usually covered, when it may not be, what to check in your policy, and what to do after the damage happens. For a broader view, it also helps to understand what car insurance usually covers before you file a claim.

Quick answer

Does car insurance cover windshield replacement? It often does if you have comprehensive coverage and the damage was caused by something other than a crash, such as road debris, falling objects, vandalism, or weather. If the windshield was damaged in an accident with another car or object, collision coverage may be the part of the policy that applies instead. If you only carry liability insurance, your own windshield replacement is usually not covered.

How windshield replacement coverage usually works

Insurance usually looks at the cause of the damage first.

- Comprehensive coverage often applies when the windshield is damaged by something like a rock, hail, vandalism, or a falling branch.

- Collision coverage may apply when the windshield is damaged during a crash.

- Liability-only coverage usually does not pay to replace your own windshield.

This is one reason many drivers compare collision vs comprehensive insurance when they are trying to understand glass claims. The type of event matters more than the glass itself.

Another important detail is that insurers may treat repair and replacement differently. A small chip that can be fixed may be handled more easily than a long crack that requires a full windshield replacement. In some situations, the insurer may prefer repair if it is still safe and possible.

When windshield replacement is usually covered

Coverage often applies in situations like these:

- A rock or road debris hits the windshield while you are driving.

- Hail or another weather event breaks or badly cracks the glass.

- A tree branch or other object falls onto the windshield.

- Someone vandalizes the vehicle and breaks the glass.

- A crash damages the windshield and you carry the right coverage for that accident.

Even in these situations, the policy may still include conditions. For example, the insurer may ask whether the damage happened recently, whether the claim was reported quickly, and whether the glass can still be repaired instead of replaced.

When windshield replacement may not be covered

Windshield replacement may not be covered, or may be only partly covered, in situations like these:

- You only have liability insurance.

- The damage falls below your deductible, so insurance does not actually pay.

- The claim is related to wear, poor maintenance, or old damage that was never fixed.

- The insurer believes the glass could have been repaired sooner but the problem got worse over time.

- The policy has exclusions or special terms related to glass coverage.

This is where many drivers get surprised. They hear that “insurance covers windshields,” but the real answer is often more limited: the policy may help, but not every time and not always without out-of-pocket cost.

Deductible, repair, and replacement: why the final cost can change

One of the biggest questions is not just whether the claim is covered, but whether it makes financial sense to use insurance. If your deductible is high, a windshield claim may result in little or no payment from the insurer. That is why it is important to know how a deductible works in car insurance before you decide what to do.

Some policies or endorsements may treat glass differently from other comprehensive claims. For example, a policy may have a lower glass deductible, or in some cases a special glass provision. But these details vary by insurer, policy form, and sometimes by state. The safest approach is to check the exact wording in your own policy documents.

It also helps to ask one practical question: Is the windshield being repaired or fully replaced? A small repair is usually less expensive and may be easier to approve. Full replacement is more likely to raise questions about deductible, original equipment, calibration, and shop options.

What to check in your policy

Before assuming the claim is covered, review these points:

- Do you carry comprehensive coverage?

- If the damage happened in a crash, do you carry collision coverage?

- What is your deductible for the part of the policy that may apply?

- Does the policy mention glass coverage, full glass coverage, or a special endorsement?

- Does the insurer have rules about repair vs replacement?

- Are there requirements about approved shops, inspections, or claim timing?

If you have a declarations page and a full policy copy, look at both. The declarations page shows which coverages you bought, while the policy wording explains how those coverages work in real situations.

What to do after windshield damage

If your windshield is cracked or shattered, a simple process can help:

- Take clear photos of the damage as soon as possible.

- Write down what happened, including date, place, and likely cause.

- Check whether the damage looks repairable or whether visibility and safety are affected.

- Review your policy for comprehensive, collision, glass terms, and deductible.

- Contact the insurer and ask how the claim would be handled before authorizing work.

- Ask whether calibration, aftermarket glass, or shop choice affects coverage.

If the crack is spreading or blocking your view, do not wait too long. Even when coverage exists, delay can make the situation harder to document and may turn a small repair into a full replacement.

Frequently asked questions

Is windshield replacement always covered by comprehensive insurance?

No. Comprehensive coverage often helps, but payment can still depend on the cause of loss, deductible, and policy wording.

Will liability insurance pay for my windshield replacement?

Usually no. Liability coverage generally pays for damage you cause to others, not for damage to your own vehicle.

Does a chipped windshield count as a claim?

It can. Some chips are repaired through a glass claim, while others may be paid out of pocket if insurance would not help much after the deductible.

Is repair different from replacement under insurance?

Often yes. A repair may be easier and cheaper, while full replacement may trigger more policy conditions and a deductible.

Can a crash-related windshield claim fall under collision instead of comprehensive?

Yes. If the windshield was damaged during an accident, collision coverage may be the part of the policy that applies.

Should I file a claim for windshield damage?

That depends on your coverage, deductible, and the size of the loss. It helps to compare the likely insurance payment with the repair or replacement cost before deciding.

Conclusion

Car insurance may cover windshield replacement, but the answer usually depends on the cause of the damage, the coverage on your policy, and whether a deductible applies. In many non-crash situations, comprehensive coverage is the part most drivers rely on. In crash situations, collision coverage may be more relevant. Liability-only policies usually do not help with your own windshield.

The best next step is to review your policy and confirm whether the damage fits the coverage you bought. That gives you a clearer idea of whether the claim is likely to help and what details matter before the windshield is repaired or replaced.