What does car insurance cover? In most cases, the honest answer is: it depends on the policy and the coverage you carry. That is why this topic confuses so many drivers. People often assume insurance is one all-purpose protection, but a real auto policy is a bundle of separate coverages, and each one applies to different types of loss.

Many drivers only start asking this question after something goes wrong. Maybe they were hit in a parking lot, woke up to hail damage, had a windshield crack on the highway, or found out the at-fault driver had little or no insurance. At that point, the key issue is no longer “Do I have insurance?” but “Which part of my insurance applies here?” If you want the basic foundation first, see What Is Car Insurance and How Does It Work?.

This guide explains what does car insurance cover in practical terms, when different coverages usually apply, when they may not apply, what to check in your policy, and what steps to take after an incident. State rules and policy wording can vary, so think of this as a clear educational overview rather than a guarantee of coverage in every case.

Quick summary

- Car insurance can cover injuries, property damage, or damage to your own vehicle, but only when the situation matches the coverages on your policy.

- Liability usually helps when you cause damage or injuries to others, while collision and comprehensive may help protect your own car in different ways.

- Medical coverages such as MedPay or PIP can help with medical costs, depending on your state and policy setup.

- Insurance usually does not cover routine maintenance, wear and tear, or mechanical failure unless a sudden covered event caused the damage.

- Your declarations page, limits, deductibles, exclusions, and endorsements are the most important places to check before assuming a loss is covered.

What car insurance covers in general

In general, car insurance helps cover financial losses tied to accidents, injuries, theft, or vehicle damage when the event falls within the rules of the policy. That means insurance is usually designed for sudden, accidental, or specifically insured events, not for every cost of owning a car.

For example, if you cause a crash and damage another person’s vehicle, one part of the policy may help pay for that. If your own car is damaged in a collision, a different part of the policy may apply. If the damage comes from hail, theft, vandalism, or a falling tree branch, another coverage may be the relevant one. The key point is that the answer to what does car insurance cover depends on the type of incident and the protection you actually purchased.

That is also why drivers sometimes misunderstand “full coverage.” It is a common phrase, but not a precise legal definition. A broader explanation of that difference is in Liability vs Full Coverage. Even a broader policy can still have deductibles, limits, exclusions, and situations where coverage is reduced or denied.

How coverage works in real life

Even when a policy is active, coverage is not automatic just because something happened. What usually happens is more structured than people expect.

- An incident happens.

This might be a crash, theft, hailstorm, vandalism, animal strike, or another sudden loss. - You report the event.

You or another party notify the insurer and explain what happened. - The insurer reviews the policy.

The company checks the active coverages, the date of loss, the vehicle, the driver details, and whether exclusions may matter. - The facts are compared to the policy.

The insurer looks at how the damage happened and whether that type of loss fits the coverage purchased. - Limits and deductibles affect the result.

Even if the loss is covered, the final payment can still be limited by a deductible, policy cap, or other rule.

So the practical answer to what does car insurance cover is not just “accidents.” It is “covered losses that fit the policy language.” If two people have different coverages, they can have very different claim outcomes after similar events.

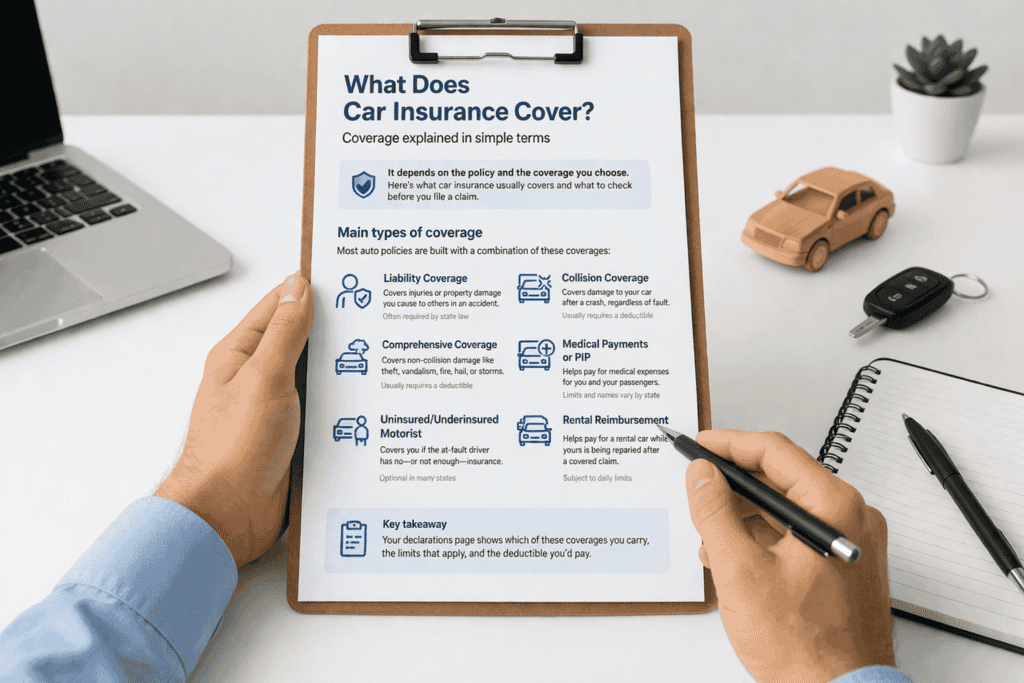

The main types of car insurance coverage

Most auto policies combine several coverages, and each one is built for a different kind of risk.

Liability coverage

Liability coverage usually helps pay for damage or injuries you cause to other people. It often includes bodily injury liability and property damage liability. This is the part of the policy that is required in most states for legal driving.

Liability coverage generally does not repair your own car. It is designed to protect you financially if you are legally responsible for harm to others.

Collision coverage

Collision coverage may help pay for damage to your own vehicle after impact with another vehicle or object. Backing into a pole, hitting a guardrail, or crashing into another car are common examples. Collision usually comes with a deductible. To understand how that affects payment, see how a deductible works in car insurance.

Comprehensive coverage

Comprehensive coverage usually applies to non-collision damage. That can include theft, vandalism, fire, falling objects, hail, animal strikes, and some weather-related losses. Many drivers think comprehensive means “everything,” but it still has boundaries and exclusions.

If you want a direct comparison between the two main physical-damage coverages, review Collision vs Comprehensive Insurance.

Medical Payments or Personal Injury Protection

MedPay or PIP may help with medical expenses for you and your passengers after an accident. The details vary by state and policy. In some places, these coverages are narrow. In others, they may be broader and more important in the claim process.

Uninsured or underinsured motorist coverage

This coverage may help if the at-fault driver has no insurance or not enough insurance. Depending on the state and policy language, it may apply to injuries, vehicle damage, or both.

When car insurance usually applies

Many drivers want practical examples, not just coverage labels. In everyday terms, car insurance usually applies when the event is sudden, accidental, and fits the policy you carry.

- You cause a crash and another driver’s car is damaged.

- Your parked car is hit and your policy includes the relevant protection.

- Your vehicle is stolen or vandalized and the policy includes comprehensive coverage.

- A hailstorm damages the hood, roof, and windshield.

- You hit a deer at night and the incident fits comprehensive coverage.

- You or your passengers need medical care after a covered accident, depending on the medical coverages on the policy.

In all of those examples, the event itself is not enough. The policy still has to match the loss. That is why a covered weather loss, a covered theft loss, and a covered collision loss are not handled under the same section of the policy.

When car insurance may not apply

Knowing what may not be covered is just as important as knowing what usually is. Many problems connected to a car are still not insurance claims.

- Routine maintenance such as oil changes, tires, brake pads, and normal upkeep

- Wear and tear from age or regular use

- Mechanical failure that was not caused by a covered event

- Intentional damage

- Damage that falls within a policy exclusion

- Certain uses of the vehicle that the policy does not allow or rate properly

For example, an engine that fails because of age and poor maintenance is usually treated very differently from engine damage caused by a sudden flood or another insured event. A stolen laptop left inside the vehicle may also raise a different coverage question than damage to the vehicle itself.

What affects what is covered

The answer to what does car insurance cover is shaped by a few key details:

- Coverage types: You must carry the right protection for that kind of loss.

- Limits: A policy can cover a loss and still cap how much it pays. You can review more in this guide to policy limits.

- Deductibles: A covered physical-damage claim may still require you to pay part of the loss first.

- Exclusions: Policies spell out situations that may not be covered.

- Endorsements: These can modify standard policy terms.

- State rules: Some coverage questions are influenced by state-specific laws and claim rules.

- Who was driving and how the vehicle was used: Driver status and vehicle use can matter more than people expect.

If you are trying to figure out your own policy, the best starting point is usually your car insurance declarations page. That is where you can quickly confirm the active coverages, listed vehicles, limits, and deductibles.

What to check in your policy before assuming you are covered

Many claim surprises come from skipping this step. Before assuming that insurance will pay, check:

- Which coverages are active on the declarations page

- The liability limits on the policy

- The collision and comprehensive deductibles

- Whether the driver and vehicle are listed correctly

- Any exclusions or endorsements that change standard coverage

- Whether the type of incident matches the coverage section you expect to use

In practice, many drivers think they have a “coverage problem” when the real issue is that they never checked which specific protections were actually on the policy.

What to do after an incident if you are not sure what is covered

If something happens and you are unsure which coverage applies, a calm process helps more than guessing.

- Make sure everyone is safe and get medical help if needed.

- Take photos and note the time, location, and basic facts.

- Keep receipts, report numbers, and contact information.

- Review your declarations page to confirm which coverages exist.

- Report the loss and describe the event clearly.

- Ask which part of the policy is being reviewed and whether a deductible applies.

If you want a fuller breakdown of what happens after reporting a loss, this guide to the car insurance claims process explains the step-by-step flow.

Common misunderstandings about what car insurance covers

“If I have insurance, every accident is covered.”

No. Coverage depends on the policy, the coverage type, and the facts of the event.

“Insurance covers any damage to my car.”

No. Damage to your own vehicle often depends on whether you carry collision or comprehensive coverage.

“Insurance covers mechanical problems.”

Usually no, unless a sudden covered event caused the damage.

“Insurance always covers personal items stolen from the car.”

Not necessarily. Personal belongings may fall outside auto coverage and may involve a different type of policy.

“If someone else is driving, my insurance never matters.”

No. In many situations, the vehicle’s policy can still matter, although driver permission, exclusions, and other policy details may affect how coverage applies.

The bottom line

So, what does car insurance cover? Usually, it covers specific financial losses tied to accidents, injuries, theft, or vehicle damage when the event fits the coverages listed in the policy. Liability may protect you when you cause harm to others. Collision may help repair your own vehicle after a crash. Comprehensive may help with non-collision damage like theft, hail, or vandalism. Medical and uninsured-driver coverages can fill other important gaps.

The most important thing to remember is that insurance is not one blanket promise. It is a set of protections with clear boundaries. The smartest way to avoid confusion is to check your declarations page, understand your limits and deductibles, and know which type of loss each coverage is designed to handle.

That way, when something unexpected happens, you are not just hoping the policy works. You already know what to check.

Related topics

- Car Insurance Declarations Page (Dec Page)

- Car Insurance Claims Process: 9 Steps That Really Happen

- Collision vs Comprehensive Insurance

FAQ

Does car insurance cover weather damage?

It may, but usually only if the policy includes comprehensive coverage and the damage fits the policy terms.

Does car insurance cover someone else driving my car?

Sometimes, but it depends on permission, policy wording, driver status, and possible exclusions.

Does car insurance cover engine failure?

Usually not when the problem is normal mechanical failure or wear and tear. It may be different if a covered event caused the engine damage.

Does car insurance cover a stolen car?

It may, but usually only if the policy includes comprehensive coverage and the claim fits the policy requirements.

Where should I look first to see what my policy covers?

Your declarations page is usually the best starting point because it shows the active coverages, limits, deductibles, vehicles, and listed drivers in one place.