If a household driver not listed on a car insurance policy regularly uses the car, that can create problems after a claim. Insurers often expect drivers in the same home to be disclosed when they have ongoing access to the vehicle, even if they are not the owner. To understand why that matters, it helps to know the difference between a named insured and a listed driver.

What happens next depends on the policy language, the person’s relationship to the household, how often they drive, and whether the insurer would have wanted that person added, rated, or excluded. In many cases, the issue does not come up until after an accident or another loss, when the insurer starts reviewing who was using the vehicle.

This article explains why insurers ask about household drivers, when leaving someone off the policy may become a problem, how claims may be affected, and what to review if someone in your home regularly drives the car but is not listed.

Quick summary

- A missing household driver may lead to extra claim review.

- The biggest issue is usually regular use, not one-time borrowing.

- Some claims may still be covered, but the process can become more complicated.

- The insurer may change the premium, require the driver to be added, or question coverage.

- Policy wording, exclusions, and household use details often matter more than assumptions.

- Checking the driver list before a claim is usually easier than fixing the issue afterward.

Why insurers ask about household drivers

Car insurance is priced partly on who is likely to drive the vehicle. Age, driving record, license status, claim history, and even years of experience can affect how risk is viewed. That is why insurers often ask about all licensed or potentially licensed people living in the household.

In practice, insurers usually want to know whether someone in the home:

- has regular access to the car

- uses it for commuting, errands, or school

- is a licensed driver or permit holder

- should be rated, covered, or formally excluded

This is not just an administrative detail. It affects how the insurer evaluates the policy from the beginning. If a regular household driver is left off, the policy may no longer reflect the real driving situation in the home.

When a household driver is not listed on the policy

A missing household driver does not always mean there will be no coverage. But it can create questions the insurer did not expect to face when the policy was issued. The closer that person is to being a regular driver, the more likely the omission matters.

The claim may get more scrutiny

If that driver is involved in an accident, the insurer may ask where the person lives, how often they use the car, whether they had access to the keys, and whether they should have been disclosed earlier. A routine claim can become a longer investigation simply because the driver situation is unclear.

The insurer may treat it as a disclosure issue

If the insurer concludes that the person should have been listed, it may view the omission as incomplete information. That can lead to a policy change, a different premium, or a requirement to add or exclude that driver going forward.

Coverage may depend on how the car was being used

Many drivers assume coverage works the same for anyone who gets behind the wheel. That is not always true. Some policies may still respond to occasional permissive use, while repeated household use is a different issue. It helps to understand whether car insurance follows the car or the driver before assuming the policy automatically protects every person who uses the vehicle.

How this plays out in real life

Many of these problems show up only after a loss. That is why they catch people by surprise.

For example, an adult child may move back home and begin using the insured car several times a week. Or a partner may start driving the car regularly for work and errands. If neither person is listed and a crash happens, the insurer may review whether the policy was issued using incomplete information about who had regular access to the car.

Possible outcomes may include:

- the claim is paid after review

- the claim is delayed while the facts are checked

- the insurer changes the policy after the loss

- part of the claim is disputed

- coverage is questioned for that specific driver

- the policy is later canceled or nonrenewed, depending on timing and policy rules

This does not mean every unlisted driver leads to the worst result. A one-time borrowing situation may be very different from a person who lives in the home and uses the car every week. The more regular the access, the harder it is to treat that person as just an occasional driver.

There is also a difference between a driver who was never added and one who was intentionally removed from coverage. If the policy specifically addresses that situation, the issue may overlap with excluded driver car insurance.

Common situations that raise this issue

A spouse or partner moves in

Even if that person only drives the car a few times a week, regular access can still matter.

An adult child returns home

If that child is now living at home again and using the vehicle routinely, the insurer may expect that driver to be disclosed.

A roommate uses the car often

The issue is not limited to family members. A roommate who lives in the household and regularly drives the vehicle may still matter to the policy.

Someone borrowed the car once

This may be a different situation. Many policies treat occasional permissive use differently from ongoing household use, which is why frequency matters.

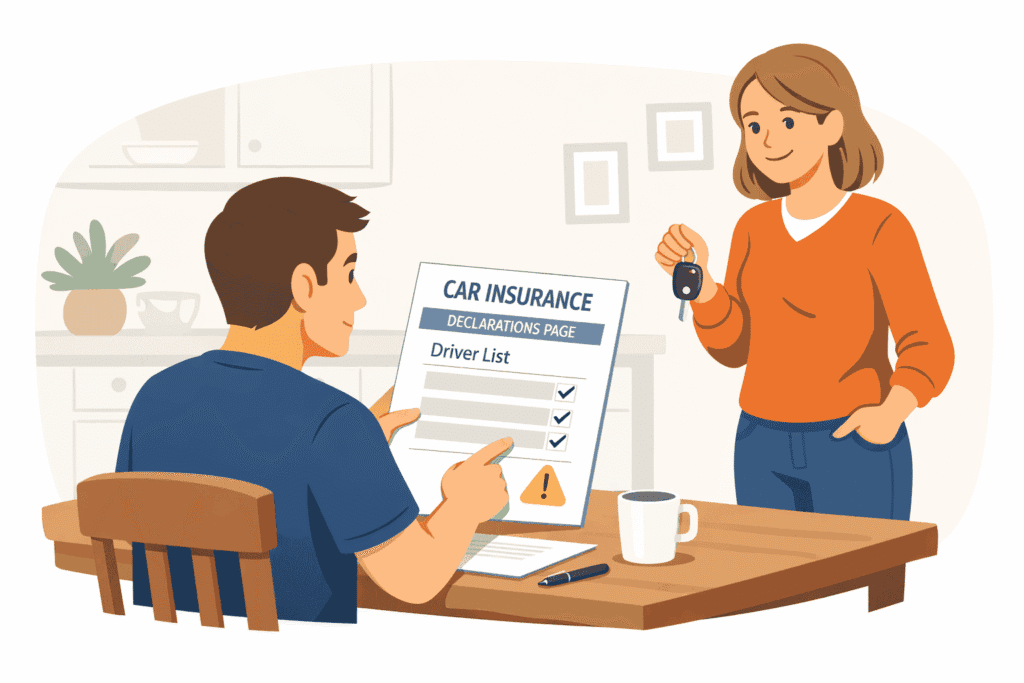

What to check in your policy

If you think someone in your home should perhaps be listed, review the policy carefully before a claim happens. Focus on the documents that explain who is covered, who is excluded, and how the insurer defines household use.

- the driver list on the declarations page

- any excluded driver endorsement

- definitions such as household member, resident relative, or permissive driver

- rules about regular use of the vehicle

- renewal forms or prior underwriting questions

It is also worth checking whether the person belongs on this policy at all. Someone who does not live with you and does not regularly drive the car may fall into a different category. In some cases, a separate arrangement may make more sense, such as non-owner car insurance.

Conclusion

If a household driver is not listed, the real risk is not just a missing name on paperwork. The bigger issue is that the policy may no longer match how the car is actually being used. That mismatch can lead to claim delays, coverage questions, premium changes, or policy action later.

Many policies treat occasional borrowing differently from regular household use, so the details matter. Reviewing the declarations page, driver list, exclusions, and household use terms can help you catch a problem early, before it becomes expensive or stressful.

Related topics

- Named Insured vs Listed Driver: What’s the Difference?

- Does Car Insurance Follow the Car or the Driver?

- Excluded Driver Car Insurance: What It Means and How It Affects Coverage

FAQ

Can a claim be denied because a household driver was not listed?

It may happen, depending on the policy wording and the facts. The main question is often whether that person was a regular household driver who should have been disclosed.

Does every person in the household need to be listed?

Not always. It often depends on whether they are licensed, live in the home, and have regular access to the vehicle.

Is occasional borrowing the same as being a household driver?

No. A person who borrows the car once in a while may be treated differently from someone who lives in the household and uses it regularly.

What should I do if I think someone is missing from the policy?

Review the declarations page and policy terms, then update the driver information before a claim happens. It is usually much easier to fix the issue early.