Collision vs comprehensive insurance is one of the most confusing parts of auto insurance, especially for drivers buying coverage for the first time. Both can help pay for damage to your own vehicle, but they cover very different types of events. If you want a simple “big picture” of how coverages fit together, start with What Does Car Insurance Cover?.

If you choose the wrong one (or skip one), you may discover after a loss that your policy does not apply. The good news is the difference is simple once you connect each coverage to the kind of damage it is meant to handle. If you’re comparing this to “full coverage,” see Full Coverage Car Insurance (and what that phrase usually means in real life).

This guide explains the difference between collision and comprehensive coverage in plain English, with real-life examples, common exclusions, and what to check on your declarations page. Insurance rules vary by state and policy, so use this as general educational information.

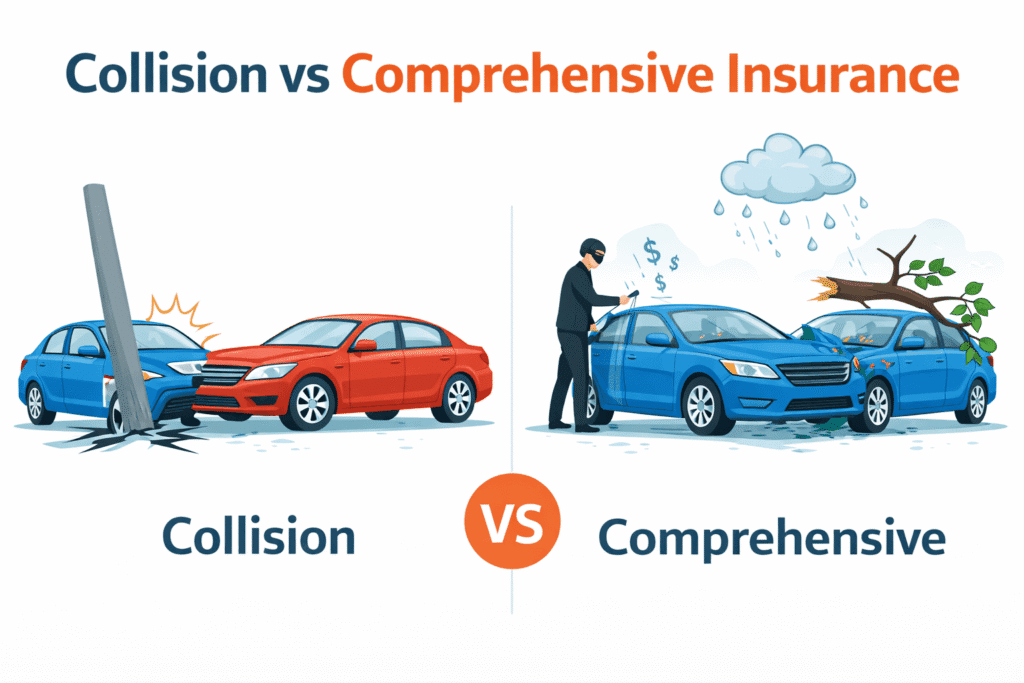

Collision vs. comprehensive: the simple definition

Collision coverage generally helps pay to repair or replace your car after it hits something (or something hits it) in a crash-type event.

Comprehensive coverage generally helps pay for damage to your car from non-collision events, like theft, vandalism, fire, hail, or hitting an animal. For a deeper dive into those non-collision losses, see Car Insurance Theft & Vandalism: What’s Covered?.

Think of it this way:

- Collision = crash damage

- Comprehensive = “other than collision” damage

For a beginner overview of what a car insurance policy is (and the main parts inside it), see What Is Car Insurance?.

What collision insurance usually covers

Collision coverage typically applies when your car is damaged in a crash, such as:

- Hitting another vehicle

- Hitting an object (like a pole, guardrail, or wall)

- Single-vehicle accidents (depending on the situation and policy terms)

- Damage caused when another vehicle hits your parked car (often handled under collision on your policy if you use your own coverage)

Collision coverage is usually optional under state law, but lenders commonly require it if you finance or lease your vehicle. If you’re unsure what coverage is required by law (versus required by a lender), see Is Car Insurance Required by Law in the U.S.?.

What comprehensive insurance usually covers

Comprehensive coverage typically applies to non-collision events, such as:

- Theft or attempted theft

- Vandalism

- Fire

- Hail, wind, or certain storm damage

- Falling objects (like a tree branch)

- Hitting an animal (like a deer)

Like collision, comprehensive is usually optional by state law, but it may be required by a lender for a financed or leased car. Most comprehensive claims also involve a deductible—see What Is a Deductible in Car Insurance?.

9 key differences: collision vs. comprehensive coverage

Here are the main differences that help you decide which coverage applies.

1) Type of event

Collision is for crash-type damage. Comprehensive is for non-collision events like theft, weather damage, and vandalism.

2) Common examples

Collision: rear-end accident, hitting a curb, sliding into a guardrail. Comprehensive: stolen car, broken window from vandalism, hail dents.

3) Deductibles

Both coverages commonly have deductibles. That means you pay a set amount out of pocket before insurance pays the rest of a covered claim. If you’re considering raising your deductible to lower your bill, see Higher Deductible, Lower Premium: 9 Clear Facts.

4) Who is at fault

Collision can apply regardless of fault when you use your own policy (your deductible may still apply). Comprehensive is usually not about fault because many covered events are not caused by another driver.

5) Total loss situations

Both collision and comprehensive may lead to a total loss decision if repair costs are too high compared to the vehicle’s value, depending on state rules and insurer guidelines. What you receive can also be limited by your policy’s numbers—see Car Insurance Policy Limits.

6) What they do NOT cover

Neither coverage is meant for routine maintenance, mechanical breakdowns, or normal wear and tear. Exclusions and conditions vary by policy.

7) Relationship to liability insurance

Liability coverage pays for damage you cause to others. Collision and comprehensive focus on damage to your own vehicle (subject to policy terms).

8) When each one is most useful

Collision is most useful when crash risk is a concern. Comprehensive is most useful when theft, vandalism, weather, or animal strikes are realistic risks in your area.

9) Lender requirements

If you finance or lease a car, your lender may require both collision and comprehensive to protect the vehicle that secures the loan.

Which one do you need?

The right choice depends on your car’s value, your budget, and your risk. Ask yourself:

- Could I afford to repair or replace my car after a crash?

- Is theft, vandalism, hail, or animal impact common where I live?

- Do I have financing or a lease that requires these coverages?

- What deductible could I realistically pay if I filed a claim?

Coverage choices affect price, but other rating factors matter too—see What Affects Car Insurance Cost?.

A helpful step is checking your declarations page to confirm whether you currently have collision, comprehensive, both, or neither. If you’re also trying to understand why your premium feels high overall, see Why Is My Car Insurance So Expensive?.

Common questions and misunderstandings

Is comprehensive the same as “full coverage”?

No. “Full coverage” is not an official legal term. People often use it to describe a policy that includes liability plus collision and comprehensive, but it can still have limits and exclusions. See Full Coverage Car Insurance.

If someone hits my parked car, is that comprehensive?

Usually no. That is typically collision-type damage. Comprehensive is for non-collision events like theft, fire, vandalism, or weather damage.

Do both cover a cracked windshield?

It depends on how the damage happened and your policy. Some windshield damage is treated under comprehensive, but rules vary by insurer and state.

Important to Know

Car Policy Answers is an independent educational website. We do not sell insurance, provide quotes, or recommend insurance companies.

This article is for general educational purposes only. Coverage rules vary by state and policy, and claim outcomes depend on the facts of the loss.