Full coverage car insurance is a phrase many drivers use to mean “I’m protected.” But after a crash, theft, or storm damage, people are often surprised to learn that “full coverage” does not automatically mean every situation is covered. If you’re starting from zero, this explainer helps: What Is Car Insurance?.

That’s because “full coverage” is not a single, official policy type. It’s a common term that usually describes a package of coverages added together, each with its own limits, deductibles, exclusions, and rules.

In this guide, you’ll learn what full coverage car insurance typically means in the U.S., what it often includes, what it may leave out, and what to check on your policy so you know what protection you actually have.

Definition / Core concept

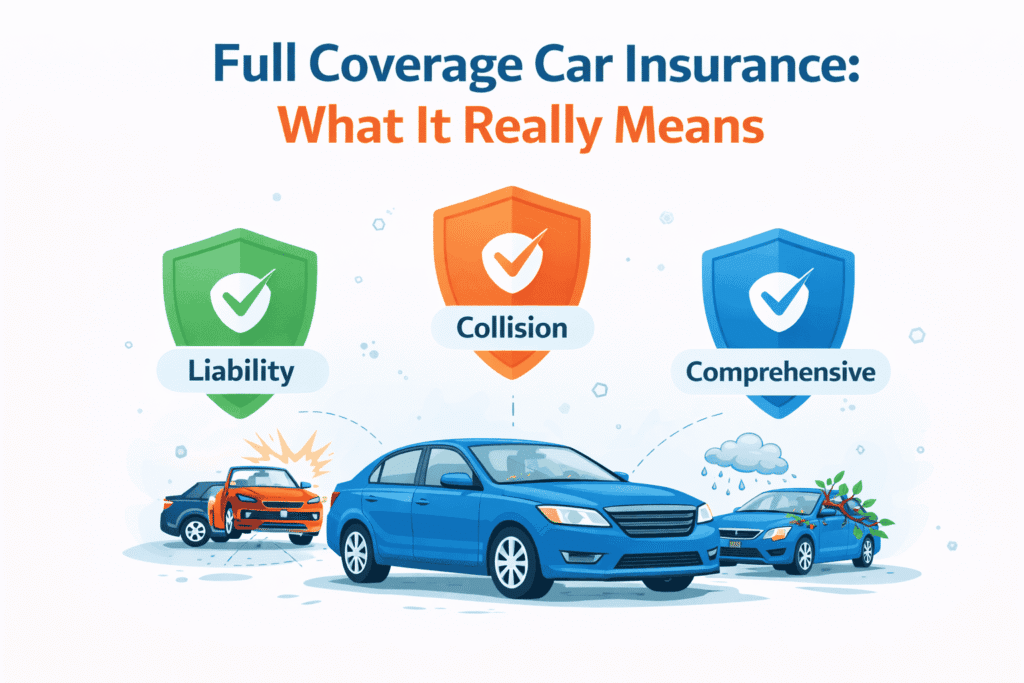

Full coverage car insurance usually means a policy that includes:

- Liability coverage (pays for injuries or property damage you cause to others)

- Collision coverage (helps pay for damage to your car from a crash)

- Comprehensive coverage (helps pay for damage to your car from non-collision events like theft or hail)

Some people also use “full coverage” to mean they added other protections (like uninsured motorist coverage or medical coverage). But those extras are not guaranteed. The only way to know is to look at your declarations page (often called the “dec page”).

Simple example: If you only have liability insurance and you crash your own car, liability typically won’t pay to fix your vehicle. Many drivers say they want “full coverage” because they want collision and comprehensive included so their own car may be covered in more situations.

How it works in practice

Full coverage is not one switch you turn on. It works as a set of separate coverages. When something happens, the claim is handled under the coverage that matches the loss.

- You choose coverages

Liability is often the starting point. “Full coverage car insurance” usually means adding collision and comprehensive. - You choose limits and deductibles

Limits are the maximum a policy can pay. Deductibles are what you pay out of pocket before certain coverages pay. - An incident happens

Crash, theft, hail, vandalism, injuries, or damage to someone else’s property. - You file a claim under the matching coverage

For example, crash damage to your car is usually collision. Theft is usually comprehensive. - The policy rules are applied

Deductibles, limits, and exclusions affect what is paid.

This is why two drivers can both say they have full coverage car insurance but have different real protection. Their limits, deductibles, and optional coverages may not match.

What full coverage car insurance usually includes

Below are the coverages most commonly associated with full coverage.

Liability coverage

Liability coverage helps pay for injuries and property damage you cause to other people. It usually includes:

- Bodily injury liability (injuries to others)

- Property damage liability (damage to vehicles or property)

Liability typically does not pay to repair your own vehicle.

Collision coverage

Collision coverage typically helps pay for damage to your car after a crash, such as:

- Hitting another vehicle

- Hitting an object (like a pole or guardrail)

- Single-car accidents (depending on the situation and policy terms)

Collision usually has a deductible.

Comprehensive coverage

Comprehensive coverage typically helps pay for damage to your car from non-collision events, such as:

- Theft or attempted theft

- Vandalism

- Fire

- Hail or wind damage

- Falling objects (like tree branches)

- Hitting an animal (like a deer)

Comprehensive also usually has a deductible.

What full coverage car insurance may NOT include

This is where many misunderstandings happen. Even with full coverage, policies commonly do not cover:

- Routine maintenance (oil changes, brakes, tires)

- Mechanical breakdowns not caused by a covered event

- Wear and tear

- Intentional damage

- Using the vehicle in ways not allowed by the policy (example: some commercial uses without proper coverage)

Also, full coverage does not remove limits. If your policy limit is lower than the total damage in a serious situation, the policy may only pay up to that limit.

Why lenders often require “full coverage”

If you finance or lease a car, the lender may require collision and comprehensive. The reason is simple: the vehicle is part of the loan agreement, so the lender wants it protected against common losses like crashes and theft.

In many cases, this is what people mean when they say they “need full coverage car insurance.” It’s often tied to financing requirements, not state law.

Common questions or misunderstandings

Is full coverage car insurance required by law?

No. Most states require liability coverage (and some states require other coverages), but collision and comprehensive are usually optional unless a lender requires them.

Does full coverage mean the insurance pays for everything?

No. Deductibles, limits, exclusions, and policy conditions still apply.

Does full coverage include uninsured motorist coverage?

Not always. Some states require uninsured motorist coverage, but in other states it may be optional. Check your policy.

Do I still pay out of pocket with full coverage?

Often, yes. Collision and comprehensive usually include deductibles. You may also have out-of-pocket costs if a loss is not covered or exceeds policy limits.

How can I confirm what “full coverage” means on my policy?

Look at your declarations page. It shows your coverages, limits, and deductibles. If collision and comprehensive are listed, you likely have what many people call “full coverage.”

Important to Know

Car Policy Answers is an independent educational website. We do not sell insurance, provide quotes, or recommend insurance companies.

The information in this article is intended for general educational purposes only. Coverage rules vary by state and policy, and claim outcomes depend on the facts of the loss.