After a crash, many drivers ask the same question: car insurance cover accidents or do you have to pay out of pocket? The answer depends on what happened and which coverages are on your policy. Some insurance pays for damage you cause to other people. Other coverage can help repair your own car. Some policies also help with medical bills. If you want a clean overview of how all the parts fit together, start with What Does Car Insurance Cover?.

This topic is confusing because “car insurance” is not one single coverage. If you want the simplest beginner explanation, start here: What Is Car Insurance?. A policy is usually made up of separate parts with different rules, limits, and deductibles. The same accident can be covered for one driver and not covered for another based on their policy choices. If you’re reviewing your coverage and see a big number but don’t know what it means, read Car Insurance Policy Limits.

In this guide, you’ll learn when car insurance covers accidents, which coverages usually apply, what can cause a denial, and the practical steps to take right after a crash in the United States.

Definition / Core concept

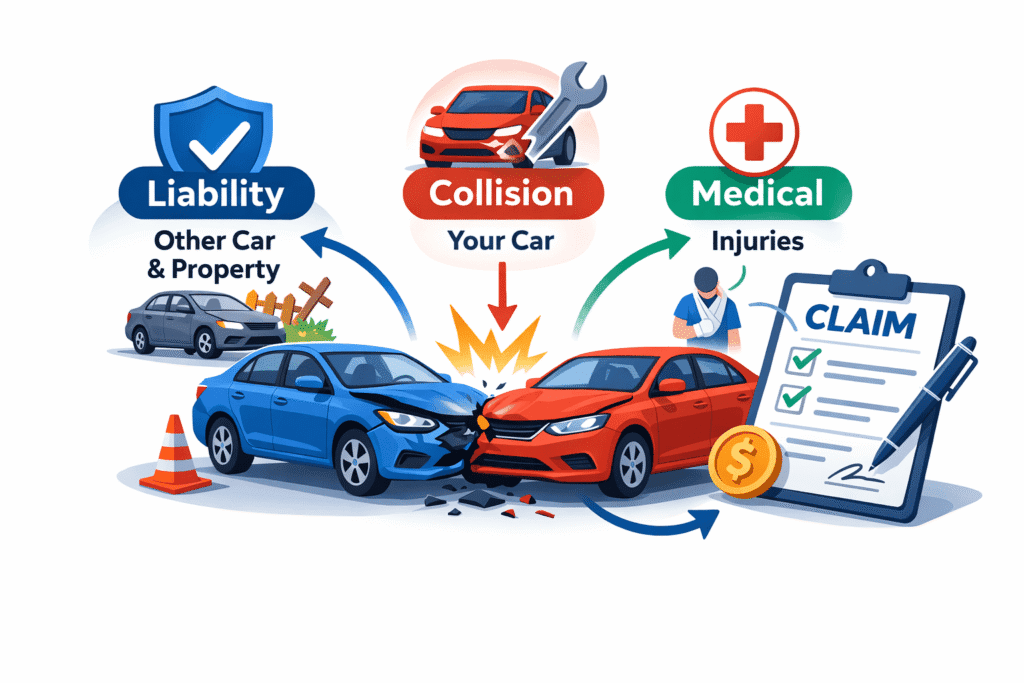

Accident coverage means your policy may pay for certain crash-related costs, but only if the accident fits your coverage and your policy terms. Coverage can apply to:

- Damage to other people (their car or property)

- Damage to your car (repairs or total loss, if you have the right coverage)

- Injuries (medical costs, depending on state rules and policy coverage)

- Legal defense (for covered liability claims, in many policies)

Simple example: You accidentally rear-end another car at a stoplight. Your liability coverage may help pay for the other driver’s repairs. If your own car is also damaged, your policy typically needs collision coverage to help pay for your repairs. To understand that “damage to your car” side, see Collision vs. Comprehensive Insurance.

How it works in practice

When an accident happens, insurers usually follow a similar process to decide whether coverage applies and what is paid.

- Report the accident

Basic details are collected: date, location, vehicles involved, and what happened. If you’re unsure what happens after you report it, see Car Insurance Claims Process. - Identify the coverages on the policy

The adjuster checks your declarations page for liability, collision, comprehensive, and injury-related coverage. - Confirm the accident facts

This may include photos, statements, police reports (if any), and repair estimates. - Match the loss to the correct coverage

- Damage you cause to others usually goes under liability.

- Damage to your car from a crash usually goes under collision (if you have it).

- Injuries may involve PIP/MedPay (depending on state/policy) and liability.

- Apply policy rules

Deductibles, limits, exclusions, and policy conditions affect the final outcome. If you’re not clear on deductibles, start here: What Is a Deductible in Car Insurance?. - Payment or repairs happen

If covered, payments are made based on policy terms and the approved amounts.

If something is not covered, the insurer typically explains the reason and points to policy language or a coverage limit. For a plain-English explanation of denials, see Can an Insurance Company Deny a Claim?.

Main types, coverage, or variations

Whether accident coverage applies depends heavily on which parts of coverage you have. Here are the main ones involved in accident claims.

Liability coverage (damage you cause)

Liability coverage generally helps pay for injuries or property damage you cause to others. It usually does not pay for your own car repairs. Many states require at least some liability coverage to drive legally.

Collision coverage (damage to your car in a crash)

Collision coverage typically helps pay to repair or replace your car after an accident involving another vehicle or an object (like a guardrail). Collision usually has a deductible. If you’re trying to lower your premium by changing deductibles, this is one of the main levers people look at.

Comprehensive coverage (non-collision damage)

Comprehensive coverage typically applies to non-collision events such as theft, vandalism, fire, hail, falling objects, or hitting an animal. It usually has a deductible. Comprehensive is not the main coverage for car-to-car accidents, but it matters for other losses that can happen around the same time.

PIP or MedPay (medical bills, depending on state/policy)

Personal Injury Protection (PIP) or Medical Payments (MedPay) may help pay medical costs after an accident. Availability and rules vary by state and policy. In no-fault states, PIP is often important because it can apply regardless of fault up to policy limits.

Uninsured/underinsured motorist coverage (when the other driver can’t pay)

If the other driver has no insurance or not enough insurance, uninsured/underinsured motorist coverage may help in some situations (often for injuries, and in some states also for property damage). State rules and policy details matter here.

Costs or influencing factors (if applicable)

No prices here, but these factors often influence what happens after an accident claim:

- Type of coverage on the policy

Liability-only policies may not pay for your vehicle repairs after you cause an accident. - Deductibles

Collision and comprehensive commonly require you to pay a deductible before insurance pays the rest of a covered claim. - Policy limits

Liability limits cap how much the policy can pay for other people’s injuries and property damage. - Fault rules in your state

Fault and no-fault rules can change how injury claims are handled and who pays first. - Accident details and evidence

Photos, statements, and repair documentation can affect coverage decisions and claim outcomes. - Policy conditions

Late reporting, lack of cooperation, or missing information can complicate a claim.

These factors help explain why two accidents that “look the same” can lead to different results for different drivers.

Common questions or misunderstandings

Does car insurance cover accidents even if I’m at fault?

Often, yes—but it depends on the coverage. Liability may cover other people’s damage. Collision may cover your car repairs if you have it, even if you caused the crash.

Does “full coverage” mean every accident is covered?

No. “Full coverage” is not a legal term. Policies still have exclusions, limits, and deductibles. Coverage depends on what is listed on your policy. Related: Full Coverage Car Insurance.

Will insurance pay for my car if I only have liability?

Usually not for your own car repairs after you cause an accident. Liability coverage is mainly for damage you cause to others.

Can an insurer deny an accident claim?

Yes, if the policy does not cover the type of loss, an exclusion applies, the policy was not active, or policy conditions were not met. See Can an Insurance Company Deny a Claim?.

Should I always file a claim after an accident?

Not always. Some minor incidents may be handled privately. But if there are injuries, major damage, or legal reporting requirements, it is usually important to document the accident and understand your policy obligations. If you want a practical checklist, see What Are Your Rights After a Car Accident?.

Important to Know

Car Policy Answers is an independent educational website. We do not sell insurance, provide quotes, or recommend insurance companies.

The information in this article is intended for general educational purposes only and is based on publicly available insurance guidelines and common industry practices.